How to Start a Business in USA as a Non-Resident

- Read & Associates

- Jan 12

- 17 min read

So, you're an international founder looking to tap into the U.S. market? It's a well-worn path, and with the right map, it's a lot more straightforward than you might think. We have helped countless founders navigate this process, and it really boils down to getting a few key decisions right from the start to ensure a compliant and scalable foundation.

Your Blueprint for U.S. Business Formation

Let's cut through the noise. Launching a U.S. company as a non-resident hinges on two fundamental choices: what kind of company you'll create and where you'll register it. These aren't just checkboxes on a form; they're strategic decisions that will dictate your taxes, legal protection, and how you operate for years to come. Getting these right is essential, as everything else falls into place much more easily.

Think of it as building a house. You wouldn't start ordering furniture before you've laid the foundation and framed the walls. The same principle applies here, and expert guidance ensures that foundation is solid.

The Two Pillars: Structure and State

Before you even think about filing paperwork, you need absolute clarity on these two points:

Business Structure: For most non-residents, the choice comes down to a Limited Liability Company (LLC) or a C Corporation. An LLC is often the go-to for its simplicity and pass-through taxation, making it a great fit for consultants, e-commerce stores, and service-based businesses. On the other hand, if your roadmap includes raising capital from U.S. venture capitalists, a C Corporation is almost always the required structure.

State of Formation: You do not have to register where you plan to do business. That’s a common misconception. States like Delaware and Wyoming are incredibly popular with international founders for good reasons, offering strong privacy protections, established corporate law, and business-friendly environments that benefit global entrepreneurs.

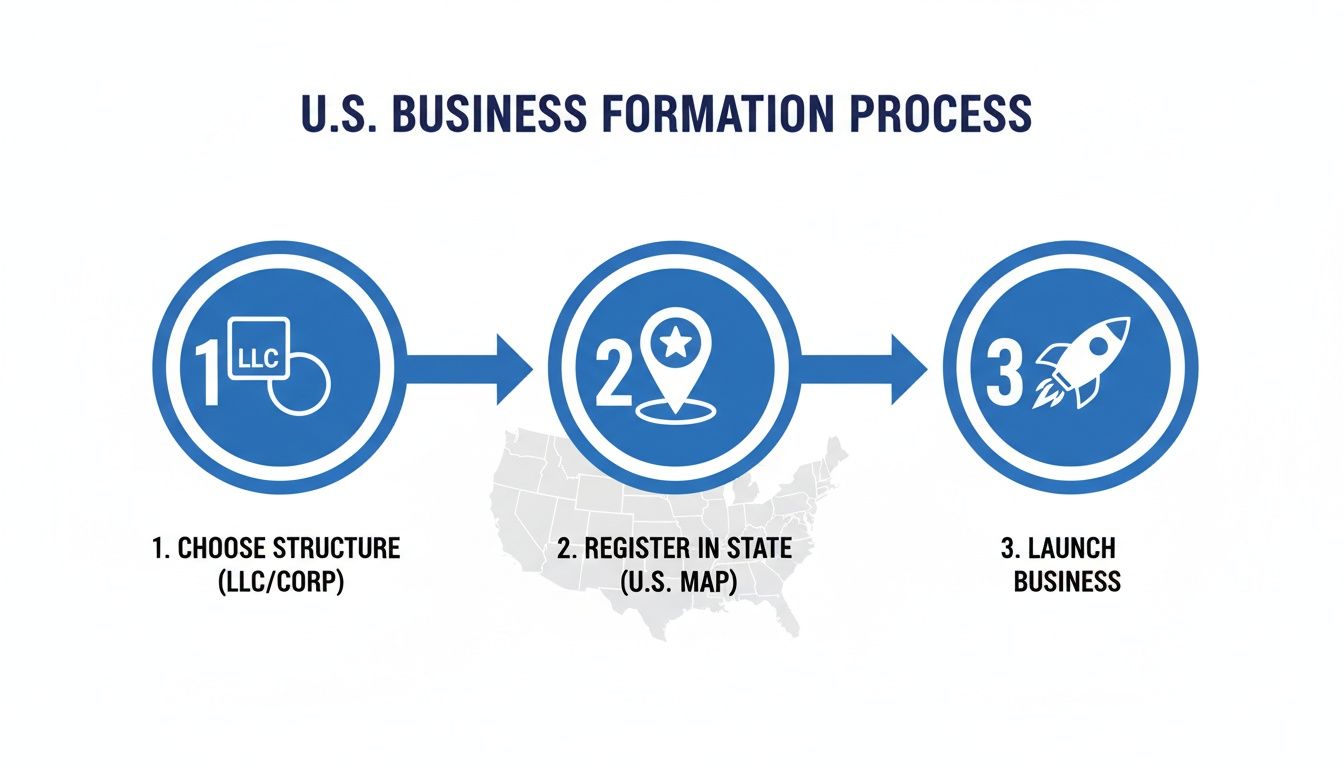

This entire journey can be simplified into a three-stage process, as you can see here.

It’s a logical flow from making those big-picture decisions to getting your company up and running and fully compliant.

To give you a clearer picture, here’s a breakdown of the critical decisions you’ll be making.

Key Decisions for Non-Resident U.S. Business Formation

Decision Area | Key Considerations for Non-Residents | Common Choices |

|---|---|---|

Business Structure | Taxation (pass-through vs. corporate), liability protection, and ability to attract U.S. investors. | LLC for operational simplicity; C Corp for VC funding. |

State of Formation | Corporate law reputation, privacy protections, annual fees, and court systems (e.g., Delaware's Court of Chancery). | Delaware, Wyoming, Nevada. |

Banking | Requirements for non-residents (some banks require an in-person visit), online capabilities, and integration with payment processors. | Mercury, Relay, Wise Business. |

Tax Compliance | Federal and state income tax, sales tax nexus, and payroll tax obligations (if hiring U.S. employees). | Work with a U.S. CPA specializing in international founders. |

These are the core elements that will shape your U.S. venture. Making informed choices here, with expert guidance, will save you significant headaches and money down the road.

Why It's a Great Time to Launch in the U.S.

You're entering a dynamic ecosystem. In 2023 alone, entrepreneurs filed a staggering 5.48 million new business applications in the U.S. That's a record-breaking figure, up nearly 50% from 2019 levels. You can dig into what's driving this trend and what it means for founders on CommerceInstitute.com.

This isn't just a random statistic. It means the infrastructure to support new businesses—especially those run by remote, non-resident owners—is incredibly well-developed. From streamlined online state portals to a whole industry of firms built to help you, the process of getting an EIN, opening a bank account, and managing taxes is more accessible than ever.

A well-planned formation isn't just about legal registration; it's about building a compliant and scalable foundation from day one. Getting the structure and state right avoids costly corrections later and positions your business for long-term success in the American market.

Getting this right from the beginning sets your company up to be not just legally sound but operationally efficient. For an international founder, that clarity and confidence are invaluable. When you’re ready to take that first step, our team is here to provide the expert guidance you need to do it right.

Choosing Your U.S. Business Structure and State

Okay, you've decided to tap into the U.S. market. Now comes the first make-or-break decision: how to structure your company and where to register it. This isn't just paperwork. It's the foundation of your entire U.S. operation, influencing everything from your personal liability and tax burden to your ability to land investors down the road.

For international founders, the choice usually comes down to two main players: the Limited Liability Company (LLC) and the C Corporation (C Corp). They are built for very different goals, so aligning your choice with your long-term vision is critical to avoid headaches and costly changes later.

LLC vs. C Corp: The Core Differences

Let’s use a real-world example. Say you're a freelance developer from outside the U.S. providing coding services to American clients. Your main concerns are protecting your personal assets and keeping taxes simple. An LLC is almost always the best fit here. It creates a legal shield between your business debts and your personal finances. Plus, it offers "pass-through" taxation by default, meaning the company's profits flow directly to you and are reported on your personal tax return. They're flexible, have fewer corporate formalities, and are perfect for solo entrepreneurs, e-commerce shops, and service-based businesses.

Now, let's flip the script. Imagine you're building a SaaS startup and your goal is to raise money from U.S. venture capitalists (VCs). In this scenario, a C Corporation is the only real option. VCs do not invest in LLCs; they invest in stock, and C Corps are designed to issue different classes of stock. This structure is what investors expect to see. It allows you to reinvest profits back into the business and signals that you're building a company for serious scale.

The decision between an LLC and a C Corp isn't about which is "better" overall, but which is better for your specific business model, funding strategy, and tax situation. A mismatch here can create significant friction as you grow.

To make it clearer, let's compare them side-by-side from a non-resident's point of view.

LLC vs. C Corporation: A Comparison for International Founders

This table breaks down the essential differences you need to consider as an international founder when choosing your U.S. business entity.

Feature | Limited Liability Company (LLC) | C Corporation (C Corp) |

|---|---|---|

Taxation | Pass-through by default; profits taxed at the owner's individual level. Can elect to be taxed as a C Corp. | Subject to U.S. corporate income tax. "Double taxation" can occur on profits and then again on dividends. |

Investor Appeal | Generally less attractive to institutional investors and VCs due to its tax structure and ownership rules. | The standard for venture capital. Can issue different classes of stock to founders, employees, and investors. |

Ownership | Highly flexible. Can be owned by individuals, other corporations, or trusts, both foreign and domestic. | Owned by shareholders. No restrictions on non-resident ownership, making it ideal for global founders. |

Formalities | Fewer requirements. Generally needs an Operating Agreement but often no mandatory annual meetings or board. | More rigid. Requires a board of directors, shareholder meetings, meeting minutes, and corporate bylaws. |

Choosing the right structure plugs you into a massive economic engine. The U.S. is home to roughly 34.8 million small businesses, a number that has swelled by about 13% since 2019. For you, this means access to a mature ecosystem of investors, payment processors, and big-name clients—but only if you're set up correctly from day one.

Choosing the Right State for Your Business

Just as vital as your entity type is your state of formation. A common misconception is that you need to register where your customers are. You don't. For non-residents operating remotely, three states consistently come out on top for their business-friendly laws.

Delaware: This is the gold standard for C Corporations, especially if you plan to seek venture capital. Over 68% of Fortune 500 companies are incorporated here for a reason. Its respected Court of Chancery (a specialized court for business disputes) and predictable legal system make it the default choice for serious startups.

Wyoming: A fantastic choice for LLCs, particularly if you value privacy and asset protection. Wyoming was the first state to even create the LLC, and its laws offer strong protections for owners. Better yet, it has no state corporate or individual income tax and keeps annual fees low.

Florida: Another great option with no state income tax. Florida is a strong contender if you might eventually relocate to the U.S. or establish a physical presence, thanks to its booming economy and international business hubs.

Your choice of state also comes with ongoing responsibilities. Every U.S. company is legally required to have a physical address in its state of formation to receive official mail and legal notices. This is handled by a service known as a Registered Agent. You can learn all about this critical requirement in our essential guide to registered agent services for U.S. business formation.

Ultimately, the right combination of entity and state comes down to your vision. Are you building a lifestyle business or the next unicorn? Answering that question is the first step toward building a successful and compliant U.S. company, and expert advice can ensure you make the optimal choice.

Bringing Your U.S. Company to Life

Alright, you’ve picked your business structure and settled on a state. Now comes the exciting part: making it real. This is where we move from planning on paper to filing the official documents that legally create your U.S. company. It's the foundational work for everything that follows, from opening a bank account to getting paid by your first American customer.

There are a few key steps here, and they're all non-negotiable. Each one layers on another piece of your company's official U.S. presence, from giving the state a point of contact to getting your tax ID from the federal government. Let’s get into what that looks like.

Why You Need a Registered Agent

Every single LLC and corporation in the United States must have a Registered Agent. It’s a legal requirement, plain and simple. This is a person or a company with a physical street address in your state of formation who agrees to receive official mail and legal documents for your business.

For a non-resident founder, this isn't just a box to tick—it's your lifeline in the state. Since you don't have an office there, your Registered Agent serves as your official local contact, making sure you don't miss a critical tax notice from the Secretary of State or, in a worst-case scenario, a legal summons.

Think of it this way: the state needs a guaranteed way to reach your company. Your Registered Agent is that guarantee, even when you're thousands of miles away.

Filing the Formation Paperwork

With a Registered Agent on board, it’s time to file your formation documents. This is the moment your company officially comes into existence. The document you file depends on the entity you chose:

For an LLC, you'll file what’s called the Articles of Organization.

For a C Corporation, it's the Articles of Incorporation.

These forms are usually straightforward, asking for basic details like your company name, its purpose, and the name and address of your Registered Agent. Once the state gives its stamp of approval—which can take anywhere from a couple of days to several weeks—your company is legally born.

At the same time, you should be drafting your key internal document: an Operating Agreement for an LLC or Corporate Bylaws for a C Corp. This document is your company's internal rulebook. It spells out who the owners are, their ownership stakes, how profits get split, and how you’ll make big decisions.

While you don't typically file an Operating Agreement with the state, it's an absolutely essential document. It can prevent a world of pain and disputes between co-founders down the road, and most banks will ask to see it before they let you open an account.

Getting Your Employer Identification Number (EIN)

Once your company is officially registered with the state, the next critical step is getting an Employer Identification Number (EIN) from the IRS. An EIN is a unique nine-digit number that the federal government uses to identify your business for tax purposes. It's essentially a Social Security Number for your company.

You can't do business without it. An EIN is mandatory for:

Opening a U.S. business bank account.

Hiring any employees.

Filing your federal tax returns.

Signing up for payment processors like Stripe.

This is where many international founders get stuck. If you don't have a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN), you cannot use the simple online application. You have to submit the form via fax or mail, a notoriously slow process that's easy to get wrong. Getting this piece right is crucial. For a more detailed breakdown, check out our founder's guide on how to apply for an EIN number.

Setting Up Your U.S. Footprint

With the legal entity formed and your EIN in hand, the last step is to establish a professional presence in the U.S. This is about more than just paperwork; it’s about building credibility and having the tools to actually manage your business from abroad.

Two services are key here:

A U.S. Virtual Business Address: This gives you a professional mailing address that isn't just a P.O. Box. All your business mail arrives there, gets scanned, and is sent to you digitally. It's how you’ll manage correspondence from banks, clients, and government agencies without missing a beat.

A U.S. Business Phone Number: A U.S.-based number, usually through a VoIP service like Grasshopper or OpenPhone, adds another layer of legitimacy and makes it easy for American customers and partners to reach you.

Completing these steps takes you from having an idea to running a fully operational U.S. business, ready to open a bank account and start making money. It can feel like a lot to juggle, but getting this foundation right is everything. Our team handles this entire sequence for non-resident founders every day, ensuring it's done smoothly and correctly from the start.

Setting Up Your Financial and Banking Infrastructure

You’ve successfully formed your U.S. company and have the EIN in hand. That’s a huge milestone, but without a U.S. bank account, the business is really just a shell company on paper. To actually operate—to get paid, manage cash flow, and track your money properly—you need to build its financial engine.

For founders living outside the U.S., this step can feel like the most daunting part of the entire process. We've seen many entrepreneurs get stuck here. Most traditional American banks require you to walk into a branch to open an account, which is a non-starter for most. Luckily, things have changed dramatically in recent years, with a new wave of online solutions designed specifically for people in your exact situation.

Opening Your U.S. Business Bank Account

The first order of business is picking the right financial partner. While big names like Chase or Bank of America are everywhere, their strict in-person verification rules are a dead end for most international founders. This gap in the market created a perfect opportunity for modern fintech platforms to step in.

Today, companies like Mercury and Relay have become the default choice for non-resident business owners. They were built from the ground up for a digital world, offering powerful online banking services that are perfect for startups and e-commerce ventures. Their entire application process is done remotely, which is exactly what you need when you're starting a business in the USA from another country.

To get your account open, you'll need to have a few key documents ready to upload:

Articles of Organization/Incorporation: This is the official state filing that proves your company exists.

Employer Identification Number (EIN): Your business’s tax ID. If you need a refresher, our guide explains what an EIN number is and how to get one.

Operating Agreement or Bylaws: This internal document shows who owns the company and how it's managed.

Founder's Government-Issued ID: A clear, high-quality copy of your passport is usually required.

The process itself is quite simple, but the key to getting approved quickly is having all your documents organized and ready to go before you even start the application.

Crucial Tip: Never, ever mix your personal and business finances. It’s a rookie mistake called "co-mingling funds," and it can allow a court to "pierce the corporate veil," making your personal assets vulnerable in a lawsuit. A separate business bank account is absolutely non-negotiable for liability protection.

Establishing Your Accounting System from Day One

With your bank account active, do not wait to set up your accounting system. Trust us, trying to piece together your financials a year later during tax season is a nightmare you want to avoid. Get started immediately with cloud-based software like QuickBooks Online or Xero.

These platforms are more than just digital ledgers; they give you a real-time dashboard of your company's financial health. The best part is that you can connect your new U.S. bank account directly to the software, which automatically pulls in all your transactions. This one step will save you hundreds of hours of manual data entry down the road.

A clean, up-to-date accounting system lets you:

Make smart decisions based on accurate data about your revenue, costs, and profit margins.

Breeze through tax season without the last-minute panic of digging for receipts.

Look professional and organized if you ever need to show your financials to investors or lenders.

Why This Financial Foundation Matters So Much

Think of your bank account and accounting software as the central nervous system for your U.S. business. Every single dollar flows through this system. A messy setup from the start leads to confusion, compliance headaches, and missed opportunities.

For example, without proper bookkeeping, how will you know which of your products is the most profitable or where you're bleeding cash on unnecessary expenses? When it’s time to file your tax return, handing your accountant a clean set of books will save you a fortune in fees and dramatically reduce your risk of an IRS audit.

This professional financial infrastructure isn’t just about checking a box—it's a strategic advantage. It gives you the clarity and control needed to scale your U.S. operations with confidence. Our team specializes in getting these systems right for non-residents, ensuring your business is built on a solid, scalable foundation from the very beginning.

Staying Compliant: Your Guide to U.S. Taxes and Filings

Getting your U.S. company formed is a huge milestone, but let's be clear: it’s just the starting line. The real work is in the day-to-day grind of staying compliant. This is what keeps your business in good legal standing, protects you from steep penalties, and ultimately builds a company that lasts.

For founders outside the U.S., the American tax system can feel like a labyrinth. But if you get a handle on your key obligations from the get-go, you'll be able to navigate it with confidence.

We like to tell clients to think of their new business like a car. The formation process is you buying the car and getting the keys. Ongoing compliance? That's the regular maintenance—the oil changes, tire rotations, and inspections. It’s what keeps your car running smoothly and legally on the road. Skip it, and you're not just risking a breakdown; you're risking getting your car impounded.

First Up: Federal Tax Obligations

Your biggest annual task will be filing a tax return with the Internal Revenue Service (IRS). The exact form you'll use depends entirely on how your company is structured.

C Corporations: If you have a C Corp, you'll file Form 1120, U.S. Corporation Income Tax Return. For most companies operating on a standard calendar year, the deadline is April 15th.

LLCs: This is where things get a little more specific. A single-member LLC owned by a non-resident is typically a "disregarded entity." This means you'll need to file Form 1120 and Form 5472 to report any transactions that happened between the LLC and you, the foreign owner.

Pay close attention to Form 5472. The IRS is not messing around with this one. The penalty for failing to file it—or even just filing it incorrectly—starts at a whopping $25,000 per form. This is a non-negotiable requirement for foreign-owned U.S. companies.

Keeping clean, organized financial records throughout the year isn't just a "nice-to-have." It's the foundation of a stress-free tax season. When your books are tidy in a system like QuickBooks or Xero, filing your federal returns is straightforward and accurate. It saves you from a world of hurt, including expensive accounting clean-up jobs and unwanted attention from the IRS.

Don't Forget About State-Level Compliance

On top of your federal duties, you have separate obligations to the state where you registered your business. These filings are completely independent of the IRS.

The most common requirement is the Annual Report. This is usually a simple form where you confirm basic details about your company, like its current address and the names of its directors. It sounds minor, but missing the deadline can lead to penalties and, in a worst-case scenario, the state can administratively dissolve your company. That means it legally stops existing.

State income tax is another layer. This is where your choice of state really matters. States like Wyoming and Florida are popular with international founders precisely because they have no state income tax, which can simplify your financial life considerably.

The Ever-Growing Challenge of Sales Tax

If you're selling products or even certain services to American customers, you need to get familiar with a concept called sales tax nexus. Think of nexus as a significant connection between your business and a state. Once you establish that connection, you're on the hook for collecting and remitting sales tax there.

It used to be that you only had nexus if you had a physical presence, like an office or an employee. But a landmark 2018 Supreme Court decision blew that wide open. Now, states can also claim "economic nexus," which is triggered simply by your sales volume.

For instance, a state might say you have nexus if you make over $100,000 in sales or conduct 200 separate transactions with its residents in a year. With 50 states all playing by slightly different rules, this can become a massive headache for e-commerce businesses. Ignoring it is a recipe for a huge bill for back taxes and penalties down the line.

Why Smart Compliance Is Your Secret Weapon

Let's talk numbers. The data shows that about 20–21.5% of new U.S. businesses don't make it past their second year. That number jumps to roughly 45% within five years. For non-resident owners juggling the extra complexities of U.S. tax law, the risk is even higher. If you want to dig deeper, you can find more insights about these small business trends and what's behind them.

This is precisely why so many global entrepreneurs team up with U.S. compliance experts. Having a dedicated partner to handle year-round monitoring, reconcile your books, and provide proactive tax planning gives you the discipline needed to be one of the businesses that thrives past the five- and ten-year marks.

Staying on top of your compliance isn't just about avoiding trouble. It's about protecting your investment and ensuring your business remains a valuable, legally sound asset. When you’re ready to build that solid foundation, our team is here to manage the details so you can focus on what really matters—growing your company.

Questions We Hear All the Time from Founders Abroad

When you're figuring out how to start a business in the USA as a non-resident, a lot of questions pop up. It’s completely normal. Based on our extensive experience with international founders, here are some straight answers to the things people ask us most often.

Do I Really Need a Visa to Start My U.S. Company?

No. You absolutely do not need a visa or U.S. residency to own a U.S. company. The American legal system draws a very clear line between business ownership and your immigration status. You are perfectly free to form an LLC or a C Corporation and run it from your home country.

But here’s the crucial part to remember: owning the company is not the same as working for it in the U.S. To legally work on the ground in the United States, you would need a proper work visa (like an L-1, E-2, or O-1). Ownership and employment are two very different things in the eyes of the law.

Can I Actually Open a U.S. Bank Account from My Home Country?

Yes, you can, and it's much easier than it used to be. The old days of having to fly to the States just for a bank appointment are pretty much gone, thanks to modern fintech platforms.

Services like Mercury and Relay were built with remote founders in mind and have a completely online application process. Just make sure you have your company formation documents and your official EIN confirmation letter from the IRS handy before you start.

The ability to open a U.S. bank account remotely is a game-changer for international entrepreneurs. It gives you immediate access to U.S. payment gateways like Stripe and makes doing business with American customers incredibly straightforward.

What's the Realistic Budget for All of This?

Getting your budget right means looking at two different types of costs: the one-time setup fees and the yearly recurring expenses.

Here’s a practical breakdown:

One-Time Formation Costs: You should plan for a range of $500 to $1,500. This generally covers the state filing fee, your first year with a Registered Agent, and professional help to get your EIN from the IRS.

Ongoing Annual Costs: Be prepared for $1,000 to $3,000+ per year. This is for renewing your Registered Agent, filing state annual reports, and—most importantly—getting your federal and state tax returns prepared and filed correctly.

Keep in mind, these are starting figures. Your final tax preparation costs will really depend on how complex your business is and how many transactions you have. Factoring these expenses into your plan from the very beginning is the secret to keeping your U.S. company healthy and in good standing.

Diving into U.S. business formation and tax rules can feel overwhelming, but you're not on your own. The team at Read & Associates Inc. lives and breathes this stuff, providing clear, start-to-finish guidance for international founders just like you. If you’re ready to launch your U.S. business with confidence, schedule a consultation with us today.

Comments